Search

Search

Palm Oil: Growth in Southeast Asia Comes With A High Price Tag

Background

The oil palm, Elaeis guineensis, is a tropical plant said to have originated in the ancient rainforests of West Africa. Alvise Cadamosto, a Portuguese explorer, discovered the plants in the 15th century, and described them as having “the scent of violets, the taste of olive oil and a color which tinges food like saffron but is more attractive.” Today, Cadamosto’s description is probably the last one to come to mind if one is asked to size up the palm oil industry. Instead, if anyone thinks of it at all, palm oil is more likely to be associated with the mundane—hand soap, ice cream, and margarines—or the tragic—deforestation and labor abuses.

Palm oil as a vegetable oil is extracted from the mesocarp of the fruit of the oil palms, while palm kernel oil is derived from the kernel of the same fruit. One of the key differences between the two oils is related to their levels of saturated fat, with palm oil and palm kernel oil being 52 percent and 86 percent saturated, respectively. Palm oil is also used more widely in food products, such as cooking oil, shortenings, margarine, and as a feedstock for biofuel, whereas palm kernel oil is primarily used as a raw ingredient within a wide range of consumer products, including soaps, cosmetics, candles, and detergents.

An oil palm tree has an average productive lifespan of about 25 to 30 years, with fruit production starting in the third year of development. Oil palm yields reach peak levels between the eighth and tenth year, before starting a gradual decline in the 20th or 21st year. In addition to needing a steady amount of rain and sunshine, oil palms grow best in semi-tropical and tropical environments, particularly in a rainforest climate, where temperatures hover between 24 and 28 degrees Celsius.

The tropical climates in Indonesia and Malaysia are well-suited for oil palm cultivation.

Archaeological studies suggest that the oil palm was already in use as a food staple in Western Africa and highly valued by the Egyptians as early as 3,000 BCE. However, it wasn’t until the second British Industrial Revolution in the 19th century that people discovered its usefulness as a lubricant and hand soap. Even as palm oil became an internationally-traded commodity, most production remained rooted in West Africa until the early 20th century when the first commercial palm plantation was established in Malaysia.

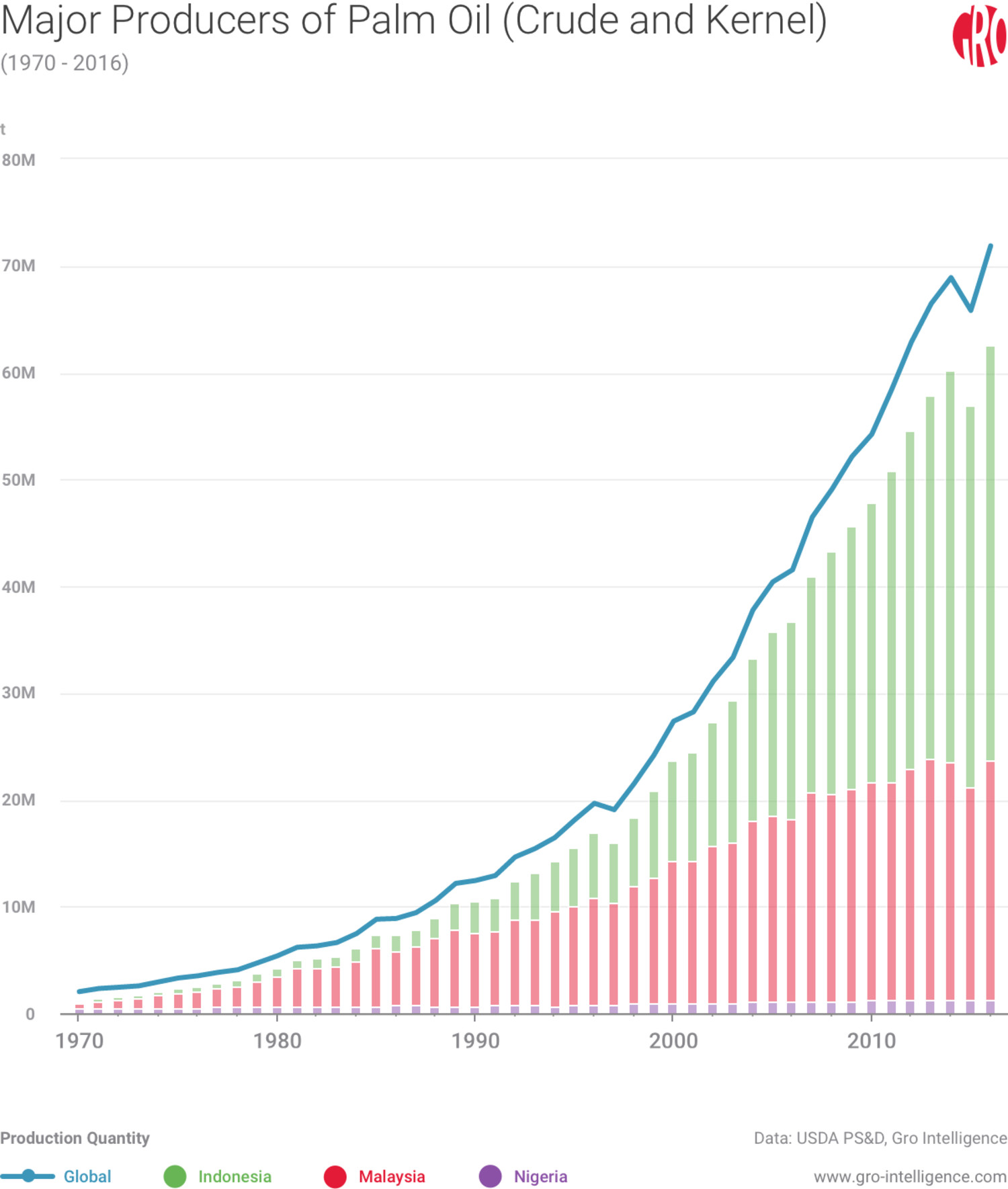

The cultivation of oil palm in Southeast Asia accelerated in the 1960s, particularly in Malaysia where the government sought to reduce the country’s dependence on rubber and tin. Production in the region has grown since the early 1960s when Africa—especially Nigeria—accounted for over 70 percent of global palm oil production. Today, Indonesia and Malaysia represent over 80 percent of global output.

Indonesia and Malaysia have come to dominate global production of palm oil, which includes both crude and kernel.

Malaysia and Indonesia have succeeded in developing a global dominance in palm oil cultivation not only because their climates are well-suited for palm cultivation. Production growth in these countries also stems from their early embrace of integrated plantation systems and large-scale, modern refineries that offer superior economies-of-scale. By contrast, palm oil production has stagnated in Nigeria, as the country’s output comes primarily from trees cultivated across dispersed and semi-wild groves, while most processing remains manual. Meanwhile, the ramp up of palm oil production, and corresponding increase in deforestation, has been accompanied by major environmental risks.

Growing consumer demand for palm oil

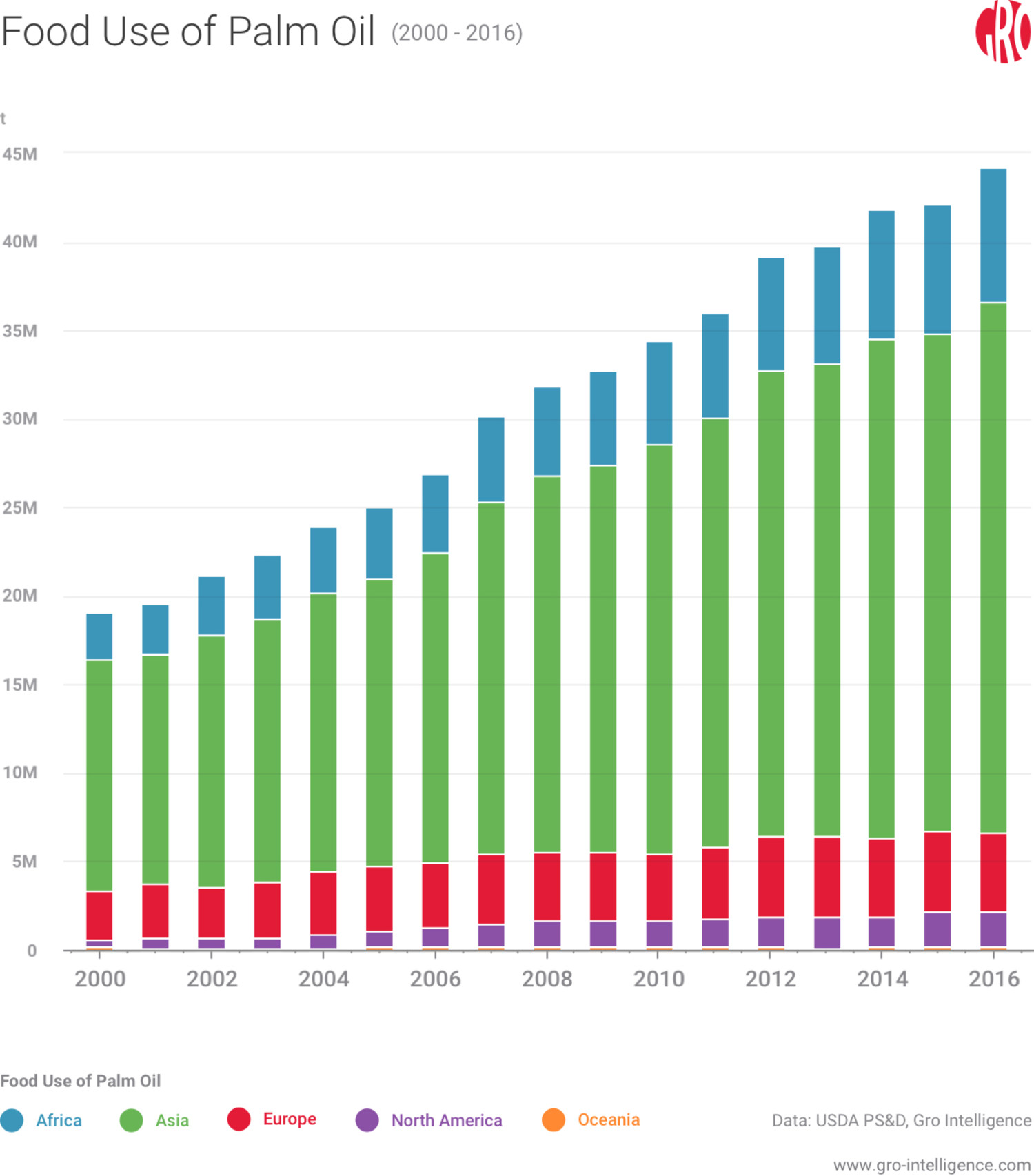

Population growth in emerging markets, global expansion by the food processing industry, and a turn away from trans fats by global consumers have all contributed to more than a doubling of the global use of palm oil for food over the past 15 years.

Although palm oil has been used as a cooking oil for centuries, it became increasingly popular as an economical source for cooking among the rapidly-growing populations of Asia and Africa. Indonesia, India, China, Malaysia, and Pakistan consumed more than half of all palm oil production in 2015.

Consumer demand drives most of the consumption of palm oil in developing countries, while biodiesel mandates make up much of the demand for palm oil in developed countries.

At the same time, the restaurant industry utilizes palm kernel oil, in particular, because it offers high oxidative stability when fried, owing to its high saturated fat content. Commercial food providers are also attracted to palm kernel oil because it is solid at room temperature, making it easy to store and transport. A growing focus on health and wellness is another reason that palm oil has experienced robust demand growth in the past decade. After health warnings of the effects of partially hydrogenated oils on cholesterol levels, food and snack processors looked for an economical substitute for oils that are free from trans fats, and they found it in palm oil. The US alone imported over four times as much palm oil products in 2015 as it did in 1999, when the FDA first proposed mandatory labeling of certain food products that included partially hydrogenated oils.

Global use of palm oil for food has significantly increased, especially in Asia and Africa.

Nevertheless, palm oil does not provide an ideal nutritional profile for consumers, in particular due to its high saturated fat content relative to other vegetable oils, especially soybean and canola. As such, some food manufacturers are using a mixture of palm oil and other vegetable oils that are lower in saturated fats to not only eliminate trans fat but also reduce saturated fat levels on the label. Soybean oil is a substitute for palm oil in some products, which translates into a close correlation between prices of the two commodities. Given that soybean oil and palm oil together account for over 50 percent of global production of vegetable oils, a drop in palm oil and/or soy oil production can have a direct impact on the input costs for a wide range of products.

These two indices provided by GEM Commodities represent a good proxy for understanding the price movements for the commodities in Northern Europe.

The European Union’s decision to establish a biofuel target—which calls for 10 percent of the energy use in the transportation sectors of each member state to come from renewable sources by 2020—provided another major catalyst for crude palm oil consumption. In fact, FEDIO, the EU vegetable oil industry association, estimates that 45 percent of palm oil used in Europe in 2014 went to biodiesel, up from just 8 percent in 2010. While European Union officials dispute these figures, they have separately estimated that the global use of palm oil use as a feedstock for biodiesel is between 10 and 15 percent. In response to growing environmental protests, the European Commission has recently decided to scrap the target for energy use in transportation after 2020.

Across Southeast Asia, meanwhile, countries have been increasing their biofuel mandate even as the concept of crop-to-fuel conversion is losing public backing in other economies. To support their domestic palm oil producers, Indonesia and Malaysia have increased the amount of palm oil that their domestic biodiesel industries are mandated to use as a feedstock for production. If Indonesia were to achieve its biofuel (B20) target in 2020, the country’s biofuel production would alone be the equivalent to nearly 20 percent of all palm oil consumed in 2015.

Can oil palm production keep growing?

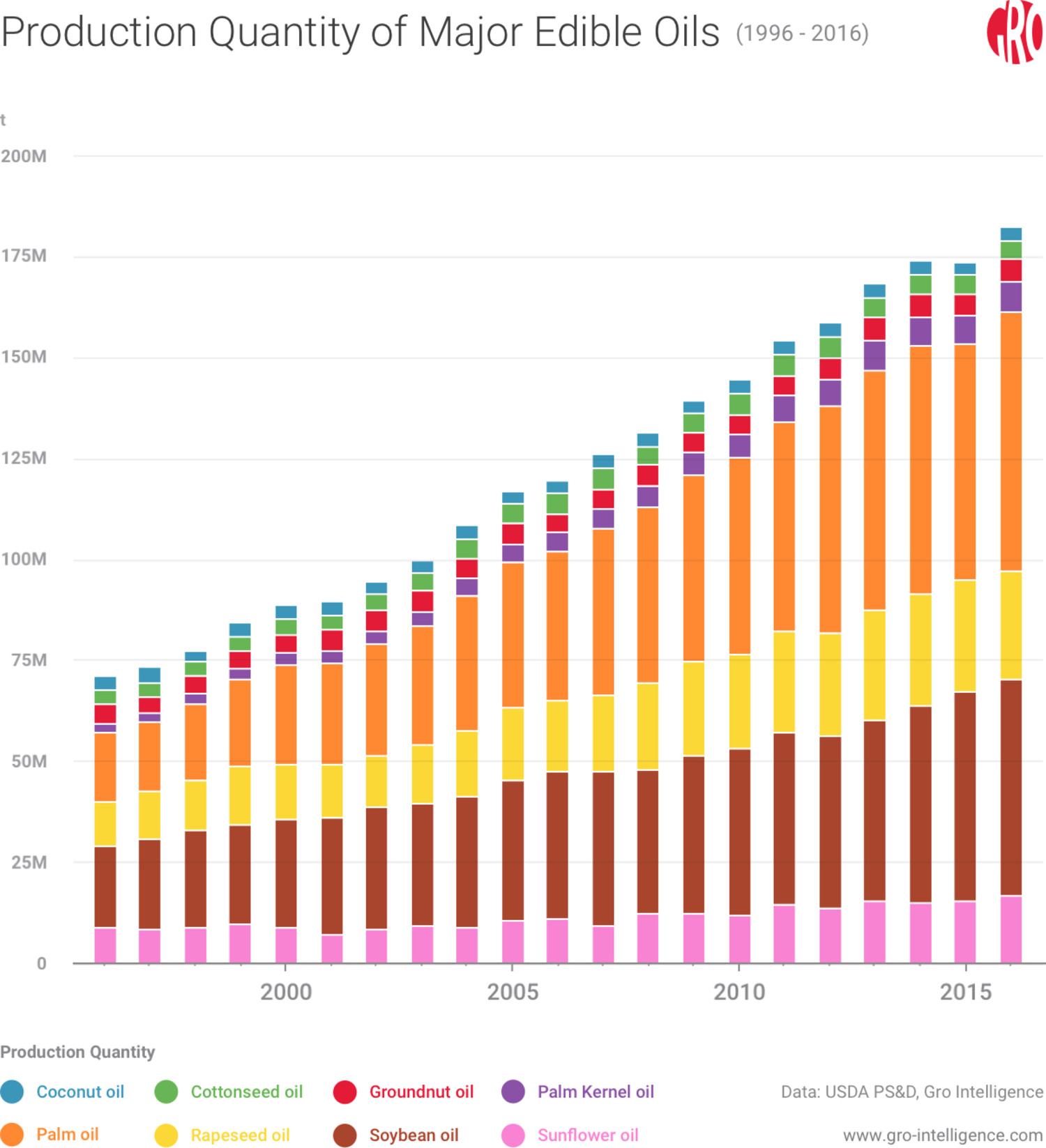

The oil palm has come to lead global vegetable oil production due to its superior oil yield profile in comparison to other oil crops.

Palm oil remains the most widely produced of all edible oils.

On average, oil palm produces nearly 4 tonnes of oil per hectare, which is roughly five times, eight times, and ten times higher than rapeseed, sunflower, and soybean yields, respectively.

Oil palm produces much more oil per hectare than rapeseed, sunflower, and soybean.

While oil palm plants can outproduce and outlive most other oil crops, productivity has begun to stagnate or even decline for the top global producers. For the last decade, most of the major palm oil producers have not been able to significantly increase their yields of oil palm fruits.

The yields of palm oil fruits have largely stagnated amongst major producers.

Agronomists have determined the optimum planting density for large-scale palm cultivation to be around 140 palms per hectare, and there is also only so much incremental production that a palm plantation operator can get out of a hectare before they have to start looking for more land. Therein lies the conundrum for palm producers who are racing to meet global demand growth. Indonesia has already seen close to 20 percent of its total forest area disappear between 2003 and 2013, due, in large part, to its expansion of palm oil production. In order to satisfy projected demand growth, industry analysts have estimated that global palm oil producers will need additional land that would be equivalent to the total area of Bangladesh (150,000 square kilometers) by 2050.

If the industry wants to satisfy projected demand for palm oil in 2050 without adding significantly more land, yields will need to rise dramatically. With this challenge in mind, the government of Malaysia announced a nationwide grower initiative in 2010 aimed at boosting average palm fruit yields by 25 percent and oil extraction rates by 12 percent in the next decade. At the moment, there is little evidence that the industry in southeast Asia has seen widespread yield improvements or is on track to reach these targets. Producers there are already at high levels of productivity, and countries have been running into labor issues, which limits near-term production potential.

The growth of palm oil production has come at the expense of rainforest areas.

Deforestation has produced an environmental backlash

In reaction to increasing deforestation, among other issues, various environmental groups and palm industry stakeholders formed the Roundtable on Sustainable Palm Oil (RSPO) in 2004 to create global certification standards for the sustainable production of palm oil. Greenpeace and other environmental organizations have seen success in recruiting global consumer product companies, including Unilever, to pledge to an increased use of sustainably-produced palm oil within their supply chains in the future. As a result, total sales of Certified Sustainable Palm Oil (CSPO) have jumped by fourteen-fold between 2008 and 2015, in no small part because of the growing influence of RSPO. Yet, with production of CPSO only accounting for less than 20 percent of global palm oil production, the industry still has a long ways to go in achieving a sustainable future.

Furthermore, sustainability groups face an uphill challenge. Global consumers, in their daily rush, don’t always find time to consider the distant impacts of palm oil production, such as the loss of rainforests (vital carbon sinks), labor abuses, and the cultivation of crop monocultures in concentrated regions. The advocacy groups may find greater success in focusing their publicity efforts on more tangible ways that consumers are being impacted by environmental changes. Global consumers are starting to realize that environmental actions in one region can influence conditions in their part of the world. In fact, consumers across Asia—a region that accounts for over 60 percent of global palm oil demand—are already seeing the impact of deforestation in the form of air pollution. In addition, Indonesia and Malaysia have each seen a roughly fivefold increase in CO2 emissions per capita between 1974 and 2013. Of course, agriculture activity is not the only culprit, but studies still show that palm oil has one of the most significant emissions profiles out of the major biodiesel feedstocks—namely soybeans, sunflower, and rapeseed.

Palm oil production, on average, emits roughly 1.5 and 4 times more CO2e per megajoule than for soybean oil and rapeseed, respectively. Indeed, the environmental damage from land use change (LUC)—which includes deforestation and peatland oxidation—is an even greater culprit than direct emissions from refining. In fact, the European Union estimates that 69 percent of gross LUC emissions for palm oil is caused by such peatland oxidation after land conversion.

CO2 emissions have significantly risen in Indonesia and Malaysia, in no small part because of deforestation.

Conclusion

A sustainable future for palm oil production remains uncertain. What is clear is that government policymakers, supply chain managers, and consumers will have to make some hard choices, and fast, to work towards a sustainable future. On the supply-side, it is hard to see how production can continue to grow at its historical pace in the region without additional deforestation in other areas, such as Papua New Guinea and the Philippines. Still, some investment groups are seeking future supply growth by returning to Africa and exploring new frontiers in South America. Benin, Colombia, Cameroon, Gabon, Ghana, Kenya, Liberia, Nigeria, and Uganda (to name a few) are countries that have either expanded existing domestic production or attracted investment from foreign investors in recent years. Nevertheless, deforestation in these countries will hardly come without an impact on the environment and local communities even if sustainable practices are incorporated into the supply chain. An alternative approach would be to limit production expansion to low-yielding pasturelands and underutilized agricultural areas, but this solution may be more difficult to enforce on a global scale.

As such, any meaningful impact will likely need to come from informed decision making on the demand side. To start, policymakers could take the lead by abolishing or strictly limiting the use of palm oil as a feedstock in biodiesel production. Reducing biofuel use would likely bring price relief to consumers who depend on palm oil and/or soy oil for their daily cooking needs. While the European Union has taken steps in this direction, a complete abandonment of biodiesel mandates in Southeast Asia is likely a non-starter, as the mandates provide price support for the domestic palm oil industry. Nevertheless, these governments could, at least, begin by requiring that all biodiesel production be CPSO certified—in spite of higher costs for domestic consumers that certification would bring—in exchange for continued support for domestic mandates.

When it comes to industry, procurement groups could substitute palm oil for more ingredients derived from soy, rapeseed, or sunflower ingredients, which are generally produced with a lower environmental (LUC) impact. Yet, the harsh reality is that even if developed countries pared back their use of palm oil, aside from biodiesel, it would only delay the inevitable. Although the current state of the palm oil industry doesn’t offer great confidence that a happy ending is in store, global supply chain managers and government policy makers can navigate towards a more sustainable future—or so we can hope.

Insight

InsightPalm Oil Price Surge Drives Global Food Inflation to 10-Year High

Insight

InsightSoybean Processors to Get a Boost as US Soy Bucks Oils Trend

Blog

BlogHow to Model Agricultural Greenhouse Gas Emissions Using Gro Data

Insight

Insight